Return to Financial Consolidation Model Overview.

A Step Acquisition refers to a business combination achieved in stages, i.e., when control is acquired through a series of equity acquisitions rather than in a single transaction. The Jedox Financial Consolidation model provides a sample configuration that demonstrates how such a step acquisition can be represented in and treated by the model. In this example, we focus on the business case in which the investor increases its investment (share) and control in an entity consolidated at equity to the extent that the entity becomes a fully consolidated subsidiary, as indicated by IFRS Foundation IFRS 3.41.

According to IFRS 3.42, the existing at equity consolidated share should be treated as if it were disposed of (fictional divestment) and accounted for at the remeasured fair value on the date of the control-gaining share acquisition. Any resulting gain or loss should be recognized in profit or loss (or other comprehensive income, as appropriate).

This fair value of the at equity consolidated share, together with the consideration transferred by the acquirer for obtaining the control-gaining share, represents the compensation for the total share of the acquirer in the subsidiary’s assets and liabilities, including goodwill (see IFRS 3.32).

After gaining control, the subsidiary’s assets, liabilities, revenues, and expenses must be consolidated into the group’s financial statements, like those of any other fully consolidated subsidiary of the group.

Representation of Step Acquisition in the Sample Data

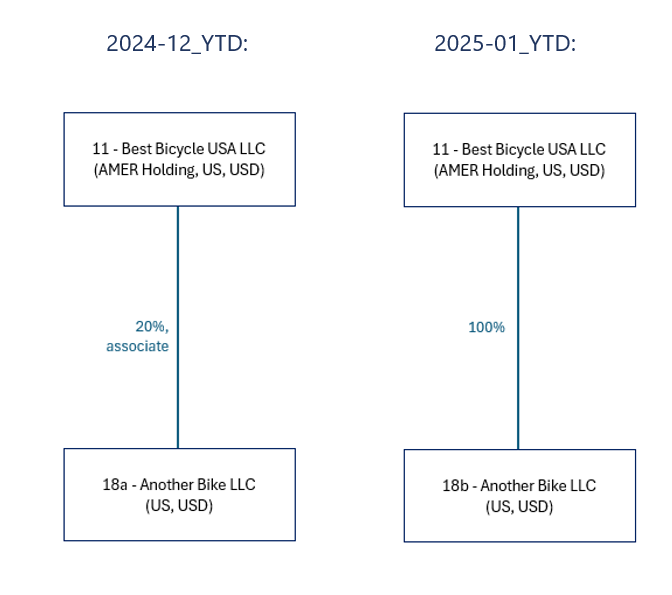

Entity 11 acquires entity 18 in stages. Entity 18 is represented with two separate legal entity codes (18a and 18b).

In the first consolidation period (2024-12_YTD), legal entity 11 (Best Bicycle USA LLC) acquires 20% of legal entity 18 (Another Bike LLC). As a result, legal entity 18 is consolidated at equity.

In the second and subsequent consolidation period (2025-01_YTD), legal entity 11 acquires the remaining 80% of legal entity 18. With this step, a control-gaining share in entity 18 is obtained. Therefore, from this point onward, the entity must be fully consolidated.

To correctly represent the fictional divestment of the at equity consolidated share of the acquired entity and avoid interferences with the consolidation of the same entity when fully consolidated, the entity is represented as two virtual entities, i.e., two separate elements in the Legal Entity and Partner Entity dimensions:

-

18afor all data of entity18when consolidated at equity -

18bfor all data of entity18when fully consolidated

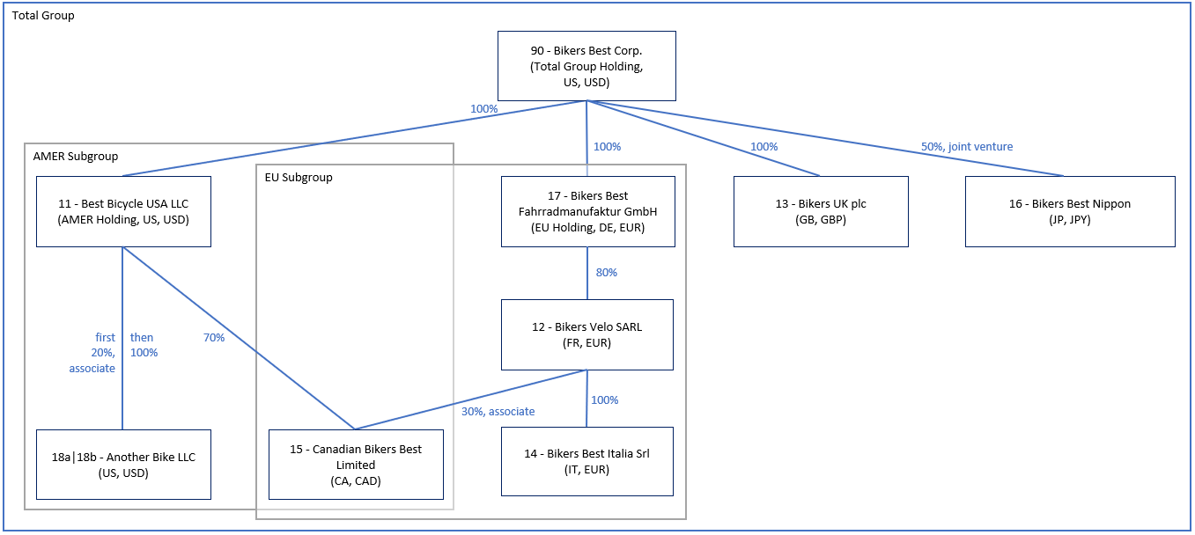

Scope and Legal Entity Structure in the Sample Data

New legal entity 18 is part of the scope of Total Group and AMER (Subgroup Americas).

Acquisition of Minority Stake in 2024

After the acquisition of 20% of entity 18 by entity 11 on 2024-12-01, entity 18 is consolidated at equity.

The representation of this business case consists of:

-

Base element

18ain theLegal EntityandPartner Entitydimensions with attribute values forName,Country(US), andCurrency(USD), included in scopesAMERandTotal Group -

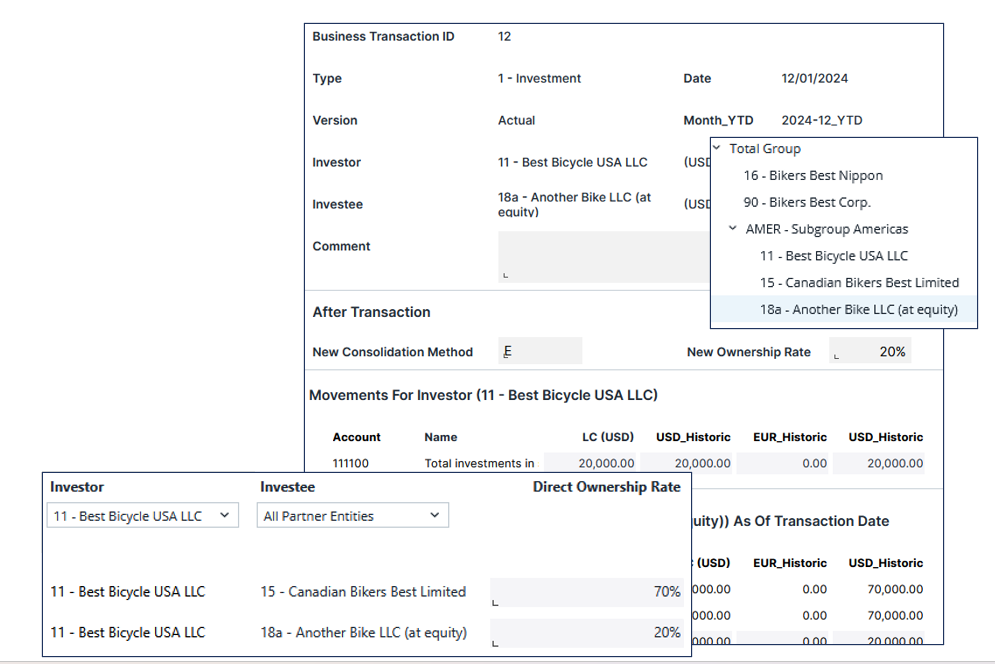

Business transaction

12with an investment amount of 20 k USD and an interim equity of entity18aof 70 k USD -

Scope of consolidation parameters for entity

18a, such as:-

Direct Ownership Rate(20%) -

Consolidation Method (E)for scopesAMERandTotal Group -

Indirect Ownership Rate(20%) for scopeTotal Group

-

-

Separate financial statements of entity

18aand an additional investment in the balance sheet of entity11

Consolidation of the Financial Figures of Entity 18 in 2024

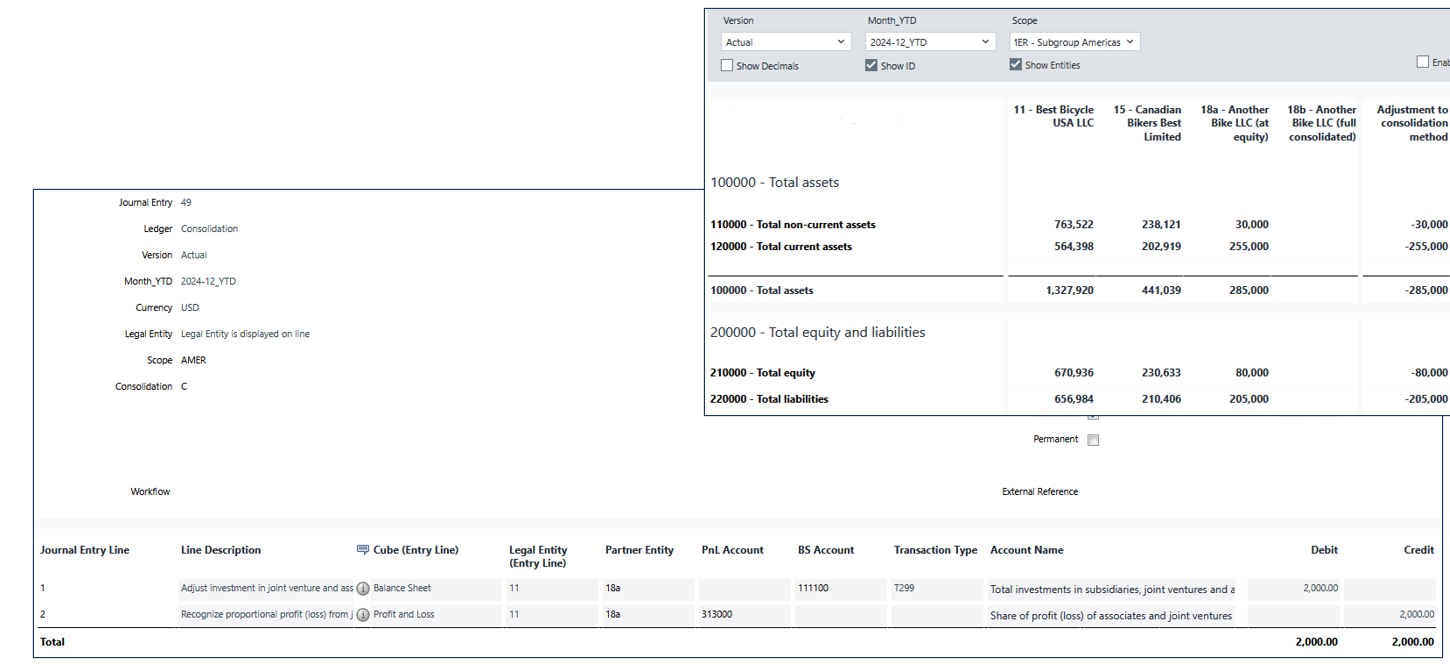

The separate financial statements of entity 18 are consolidated in 2024-12_YTD using the equity method.

The financial figures of entity 18a are consolidated in 2024-12_YTD like all other at equity consolidated entities:

-

The investment amount of entity

11of 20 k USD is not eliminated. -

All balance sheet and profit & loss values of entity

18aare eliminated via the Adjustment to Consolidation Method. -

All changes in equity of entity

18aproportionally increase the investment amount and are proportionally recognized in the corresponding equity accounts as a consolidation measure via Consolidation RuleC4.

In this example, the only change is a profit of 10 k USD. Therefore:

-

2 k USD is recognized in the P&L

-

The investment account increases by 2 k USD

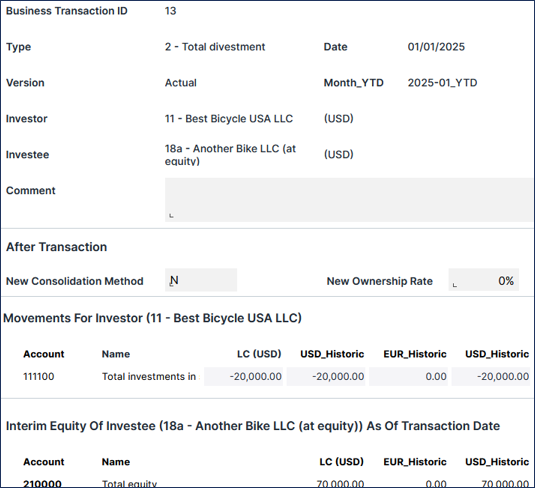

Fictional Disposal of Legal Entity 18a in 2025

To represent the remeasurement of entity 18, legal entity 18a is fictionally disposed of in 2025-01_YTD.

The divestment (fictional disposal) of entity 18a is represented by:

-

Business transaction

13of type2(Total Divestment) with:-

Investment amount of -20 k USD

-

The same equity figures as the initial investment

-

-

Scope of consolidation parameters for entity

18a, such as:-

Direct Ownership Rate(20%) -

Consolidation Method(E) for scopesAMERandTotal Group -

Indirect Ownership Rate(20%) for scope Total Group (these parameters remain active for the period of the divestment)

-

-

No movements in the balance sheet of entity

18a -

A decrease of the invested amount (20 k USD) in the balance sheet of entity

11on transaction typeT991(Outgoing Units) -

A fair value step-up (from remeasurement) of 5 k USD recognized as Gains from Divestment in the P&L of investor entity

11

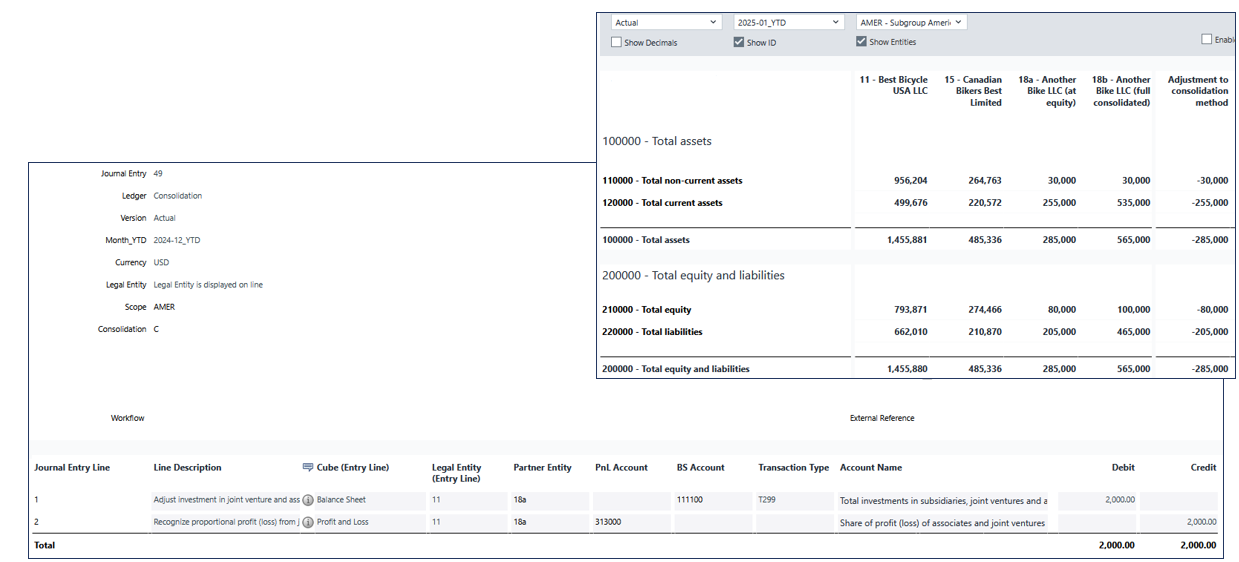

Consolidation of Financial Figures of Legal Entity 18a in 2025 (1)

The first step in consolidating legal entity 18a in 2025-01_YTD is to apply all standard consolidation measures.

The consolidation of legal entity 18a in 2025-01_YTD consists of two parts:

1. Consolidation at Equity

Including:

-

Carry forward of the previous period’s consolidation measures via Subsequent Capital Consolidation

-

Elimination of opening balances (and movements, if applicable) via Adjustment to Consolidation Method

-

Recognition of changes in equity (there are none in this example period) via Consolidation Rule

C4

2. Divestment Measures for Legal Entity 18a

This includes eliminating the remaining values in the investment account (on investor entity 11 as legal entity and investee entity 18a as partner entity) against an adjustment of Gains (Losses) from Divestment via the new Consolidation Rule C8.

In this example:

-

The P&L is adjusted by -2 k USD

-

The investment account decreases by 2 k USD

Consolidation of Financial Figures of Legal Entity 18a in 2025 (2)

The second step in consolidating legal entity 18a in 2025-01_YTD covers the divestment via the new Consolidation Rule C8.

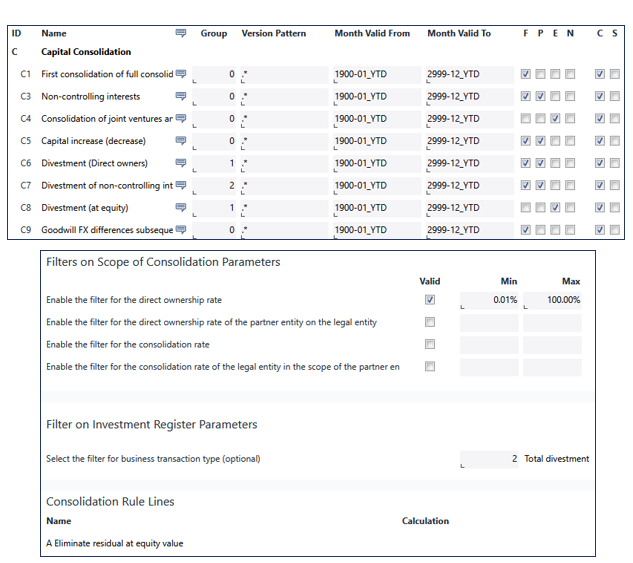

The new Consolidation Rule C8 is introduced to automate consolidation measures for total divestments from at equity consolidated entities.

This consolidation rule should be executed after other consolidation measures for at equity consolidated entities. This is achieved by assigning a higher number in the Group attribute, similar to the existing divestment rules C6 and C7.

The rule is triggered by:

-

Consolidation Method (E)

-

A filter on the

Direct Ownership Rate -

Business transactions of type

2(Total Divestment)

The rule consists of one Consolidation Rule Line that eliminates any remaining value from previous consolidation measures of a divested at equity entity in the investment account.

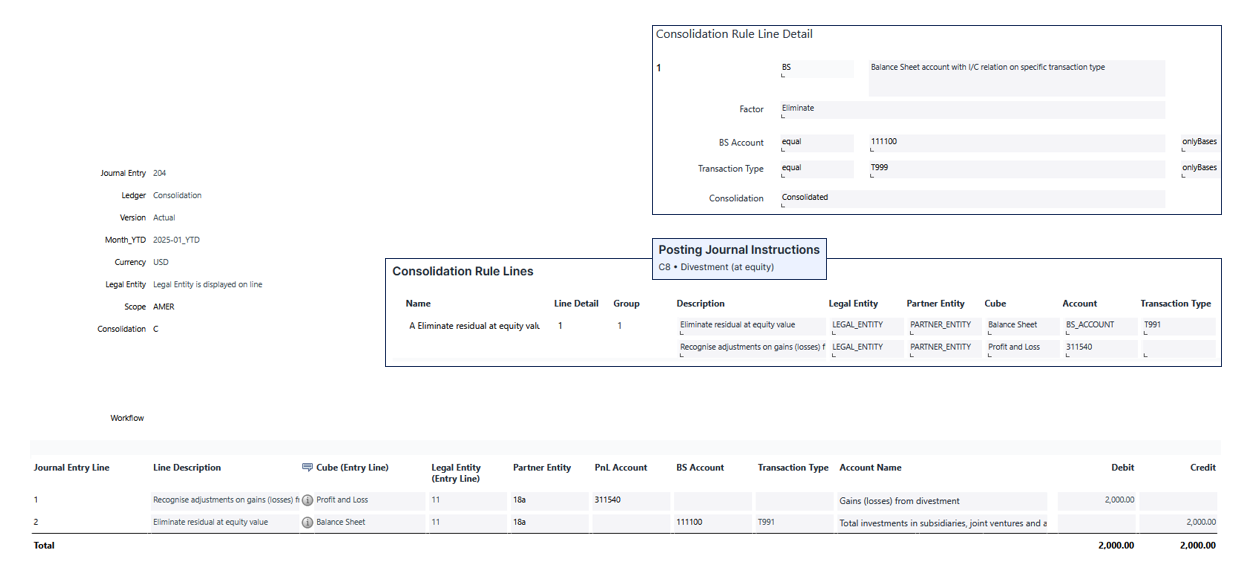

Consolidation of Financial Figures of Legal Entity 18a in 2025 (3)

The second step in consolidating legal entity 18a in 2025-01_YTD covers the divestment via the new Consolidation Rule C8.

For this purpose, the consolidation function BS is used to select values of the closing balance on the investment account and consolidation level Consolidated.

The Posting Journal Instructions indicate that a journal entry should be posted:

-

For the amount derived by fact selector

BS -

On the investment account

-

On transaction type

T991 -

Against P&L account

311540

By running the consolidation, this results in:

-

An adjustment of Gains (Losses) from Divestment of -2 k USD in the

P&L -

A decrease of 2 k USD in the investment account on transaction type

T991(Outgoing Units)

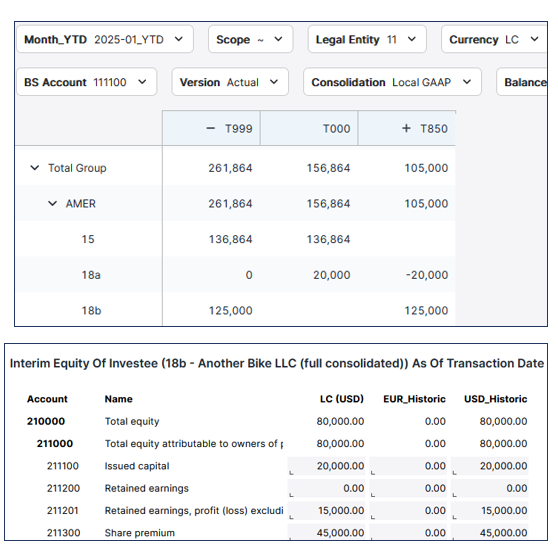

After all these measures are applied, no remaining values of legal entity 18a exist in the closing balances of the related scopes AMER and Total Group.

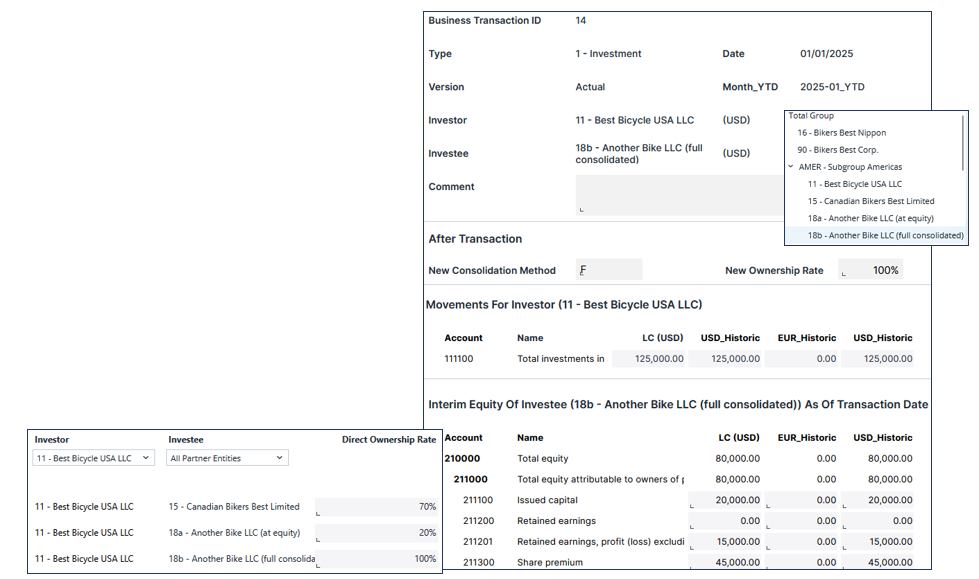

Acquisition of 100% of Legal Entity 18b in 2025 (1)

The second investment consists of acquiring the complete stake in legal entity 18b.

The representation of entity 18 when fully consolidated consists of:

-

Base element

18bin theLegal EntityandPartner Entitydimensions with attribute values forName,Country(US), andCurrency(USD), included in scopesAMERandTotal Group. -

Business transaction

14with:-

Investment amount of 125 k USD

-

Interim equity of entity

18bof 80 k USD

-

-

Scope of consolidation parameters for entity

18b, such as:-

Direct Ownership Rate(100%) -

Consolidation Method (F) for scopes

AMERandTotal Group -

Indirect Ownership Rate(100%) for scopeTotal Group

-

-

Separate financial statements of entity

18band an additional investment in the balance sheet of entity11

Acquisition of 100% of Legal Entity 18b in 2025 (2)

The consideration paid for the second investment already includes the previously acquired shares and gains from divestment.

The investment amount of 125 k USD from investor entity 11 consists of:

-

100 k USD paid consideration for 80% of entity

18, booked as investment on partner entity18bin the separate balance sheet -

20 k USD income from the fictional divestment of legal entity

18ainLocal GAAP(representing the already acquired 20% share of18b) -

5 k USD gains from the fictional divestment of legal entity

18a(step-up resulting from the remeasurement of the fair value of the already acquired 20% share of18b)

The retained earnings of the Interim Equity (from before the investment) increased to 15 k USD because of the 10 k USD profit of entity 18 in 2024-12_YTD, with no dividends paid out.

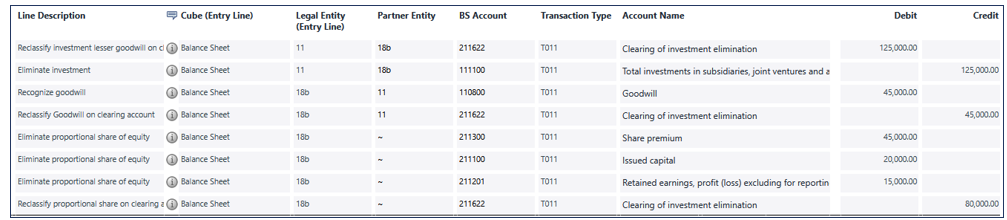

Consolidation of Financial Figures of Legal Entity 18b in 2025

The financial statements of legal entity 18b are fully consolidated in 2025-01_YTD.

The financial figures of entity 18b are consolidated like those of all other fully consolidated entities:

-

All balance sheet and profit & loss values of entity

18bare included in the Combined Financial Statement. -

The investment amount of investor entity

11of 125 k USD is eliminated as a consolidation measure via Consolidation RuleC1against:-

The elimination of the proportional equity of investee entity

18bof 80 k USD -

The resulting goodwill of 45 k USD

-

-

Consolidation measures from further Consolidation Rules would apply to any additional intercompany relationships of entity

18b(none exist in this example).

Furthermore, if the currency of the investee differs from the group currency, foreign currency exchange differences on goodwill would be recognized via Consolidation Rule C1 (not applicable in this example).

Updated May 19, 2026